Foreword

In 2021, the Intergovernmental Panel on Climate Change released a working group report that addressed the “most up-to-date physical understanding of the climate system and climate change.1 Its message was clear: human activities are damaging the environment, with every tonne of carbon dioxide emission adding to global warming.

Reports also show that supply chain emissions, which are significantly higher than the direct emissions that companies produce,2 need to be taken seriously if we are to turn the tide on climate change. In particular, companies that include transport in their supply chains must commit to using more electric vehicles (EV) now.

Although the transportation sector has always been difficult to decarbonize, especially in Canada given its climate and the size of its geography, advancement in technology is increasing the ability to introduce electric vehicles into transportation fleets. Policy changes are also slowly but decidedly moving in the right direction. As well, there is a compelling business case for companies to embrace fleet electrification due to clear cost savings on fuel, maintenance and overall operations.

Aligned to our core pillars — our customers, our company, our team and our world — this paper outlines Metro Supply Chain’s commitment to lessen the impact of our supply chain’s emissions and support our customers in reducing their own carbon footprint. Throughout our journey, which includes purchasing EV trucks and building out the infrastructure to support sustainable delivery, we have learned important insights that we hope will inform other companies as they commit to their own electrification strategies.

Introduction

Since the 1980s, scientists have been raising the alarm about the link between human activity and climate change. However, it was only recently that the climate crisis has become top of mind for business leaders.3 In January 2021, Larry Fink, BlackRock’s highly influential CEO, wrote in his annual letter4 that his fellow executives must put climate change front and centre. In April 2021, more than 400 companies, including Google, Walmart and McDonald’s, wrote an open letter5 to President Joe Biden saying that the United States should double the cuts to its existing greenhouse gas (GHG) emissions targets by 2030. Many Canadian companies, such as Canada Goose, Air Canada and the big five banks have also pledged to get to net-zero-emissions by 2050 or earlier.6

While it is certainly positive that more businesses are taking a stronger stance on sustainability, companies need to do their part now to eradicate GHG emissions from their own operations. An important area companies should focus on is the reduction of emissions generated by their supply chain, more specifically, emissions from over-the-road transportation.

A 2019 study by CDP, a non-profit organization that runs a global disclosure system for investors, companies, cities, states and regions to manage their environmental impacts, found that supply chain emissions are 5.5 times higher than companies’ direct emissions.7 In Canada, specifically, transportation accounts for at least 25% of the country’s overall GHG emissions. While that encompasses different modes of travel — passenger vehicles, trucks, buses, planes, trains and ships — in 2020, freight sources represented almost half (42%) of the total transportation emissions. That share is growing, with freight emissions expected to surpass passenger-vehicle emissions in Canada by 2030.8

Metro Supply Chain has long been committed to sustainability, with most of the decisions made as a company taking environmental, social and governance (ESG) issues into account. We also understand the transportation sector’s impact on climate change, which is why we have taken steps to reduce our own supply chain’s impact on emissions. Our goal is to flatten the GHG curve and then reverse these trends — in step with Canada’s pledge to cut overall carbon emissions by 40 to 45% (versus 2005 levels) by 2030 and help the country reach the targeted net-zero-emissions by 2050.9 To achieve that, the most effective and realistic action is an immediate transition toward electric zero-emission vehicles.

In October 2019, Metro Supply Chain became an early adopter in Electric Vehicle (EV) transportation through an acquisition of a last-mile delivery company, which, at the time, was one of only two Canadian logistics businesses to invest in class 5 electric vehicles. We incorporated these retrofitted EV trucks — as well as natural gas-powered ones — into our last-mile delivery solutions for our customers.

Continuing our EV journey, in early 2021 we purchased six heavy-duty Class 6 electric vehicles, with more to come in 2022. Over the past six months we have built out the EV charging infrastructure at two warehousing facilities (one in Montreal and one in Vancouver) and partnered with one of our major international customers to sustainably deliver its packages in these cities. Over the next three years, we will be expanding our EV infrastructure and vehicles across the country to allow more of our customers to take advantage of our zero-emission delivery program. We are committed to doing our part to reduce GHG while helping our customers reduce their carbon footprints.

While Metro Supply Chain is motivated by the climate crisis, our deployment strategy is built on a strong business case that includes cost savings on fuel, maintenance and overall operations. Furthermore, our research concluded that the electrification of the transportation sector is not just an opportunity for our company, but for all operations in our sphere.

Those insights led to the development of this white paper, which we hope will help Canadian companies learn how they can become leaders in electrifying the transportation within their supply chains. We review market trends driving EV adoption, the growing availability of appropriate vehicles and charging solutions, relevant policies, areas of government support, best practices and next steps. Our hope is that readers will come away with an understanding of the ways in which fleet electrification can benefit their businesses, customers, employees, investors, the country and, most importantly, our climate.

Policies and products pave the way

Canadians overall have been slow to adopt electric vehicles. According to Statistics Canada, just 4.6% of all vehicles in the country are electric, while approximately 7% of adults in the U.S. drive an electric or hybrid vehicle.10 With these kinds of numbers, it is no surprise that companies have also been slow to embrace EVs. In addition, several factors have weighed against the decarbonization of the transportation industry in Canada. The two largest are policy and products.

On the policy front, it has been a problem of half measures. In 2018, the federal government published new guidelines to reduce GHG emissions from heavy-duty gas and diesel trucks.11 A year later, Canada was the first country to sign Calstart’s Drive to Zero pledge,12 a commitment to convert medium- and heavy-duty commercial vehicles to zero-emissions. In 2019, the federal government introduced subsidies for zero-emission passenger vehicle purchases13 as well as a zero-emission vehicle (ZEV) charging infrastructure incentive program. The latter is a $240-million commitment through 2024 that supports deployment of charging systems for commercial and public fleets as well as light-duty passenger vehicles.14 However, despite all of that, there is yet to be a formalized national zero-emission vehicle policy for goods movement either in the heavy-duty freight sector or for last-mile deliveries.15 At the same time, the only rebates available to purchasers of medium- and heavy-duty electric trucks are at the provincial level — in Quebec16 and British Columbia.17

The most important issue is vehicle supply and the related challenge of battery development. While many manufacturers have touted plans for electric versions of their vehicles for some time, the number of commercially available electric trucks in any segment, from Class 2 to Class 8, has been minuscule.18 Those that exist are also significantly more expensive than their internal combustion-engine (ICE) counterparts, forcing would-be buyers to factor much higher upfront costs into their budgets. While demand and supply can be a chicken-and-egg dilemma, truck manufacturers have been constrained by battery technology that, until recently, has not been able to deliver enough range and power to support heavier freight applications. In addition, batteries do not perform well in cold conditions — vehicles can only get to approximately 40% of their intended range in -30 C temperatures19 — which makes adoption even more complicated for Canadian operations.

Fortunately, we are witnessing a sea of change on both fronts.

The 2021 federal election saw strong support across the board for transportation electrification.20 Our Federal Government can now build on the commitments it previously made to set a binding 2035 target for 100% electric new car and light-duty truck sales.21 In its election platform, the government stated that all medium- and heavy-duty trucks must be zero-emission (electric and hydrogen fuel-cell) by 2040, where feasible, and that the government would invest $200 million in a program to retrofit large trucks already on the road.22 If the 100% ZEV sales by 2040 requirement is formally enacted, Canada would rival California (which requires 40% of new Class 7 and 8 vehicles to be zero-emission by 2035) for the most ambitious timeline for commercial vehicle transition.

In the U.S., recent policy action to support electrification of medium- and heavy-duty vehicles at the federal and state23 levels, coupled with the formation of an industry-led National Zero-Emission Truck Coalition,24 has important implications for Canada. The most immediate: in September 2021, Quebec joined the state coalition initiative.25 More broadly, the potential impact these organizations will have on supply chain industry practices, investment in manufacturing and growth in vehicle supply south of the border is sure to spill over to Canada.

In fact, the growing availability of electric trucks with batteries capable of supporting a growing range of drive and duty cycles — from both production volumes and the number of models — is already increasing. In 2020, there were roughly 70 electric freight vehicle models from 24 companies on the market in North America. In 2021, that number has risen to approximately 85 models from more than 30 companies.26 A different analysis, which includes off-road equipment and buses as well as trucks, expects a doubling in the number of available models by 2023 compared to the beginning of 2020.27

While the market share of electric trucks is still under 1%, the playing field is getting crowded, with a mix of aggressive, well-funded startups and popular manufacturers in various stages of transformation. For example, the six trucks that Metro Supply Chain bought in 2021 are made by Lion Electric, based in Quebec, and BYD, a Chinese producer with manufacturing in the U.S. — two well-known brands that offer a variety of EVs, including Class 5 and 6 trucks. Among long-standing, heavy-duty nameplates, 2021 saw Peterbilt28 and Kenworth29 (Paccar), Volvo30 and Freightliner (Daimler)31 all having received their first Canadian orders for new Class 8 electric vehicles.

Naturally, companies will want to go with vehicles and manufacturers that meet their needs, but having greater choice is key. In Metro Supply Chain’s case, our selection process encompassed the following aspects:

- we wanted to purchase from manufacturers that had previous experience in the Class 5 and 6 vehicle range

- we sought manufacturers with experience in our climate, given the demands that cold weather has on battery performance

- we wanted access to nearby service centres

- we wanted to buy Canadian where possible

- since we still had a lot to learn about the technology, we opted to pilot with two different manufacturers’ products

With more manufacturers entering the market and existing ones increasing in scale, production volumes of medium- and heavy-duty vehicles are expected to grow quickly.32 As noted, this growth will be led by vehicle categories where current state-of-the-art battery technology — which determines range, cost and charging speed — is better suited to meet load weight and user needs. Going forward, higher volumes and further battery refinements will help reduce prices further.

To date, the market segments with the greatest penetration are Class 3, 4 and 5 vans and step vans, Class 6 medium-duty box trucks, Class 8 terminal tractors and Class 8 regional tractors.33 Typical applications for these types of vehicles include local, urban delivery, last-mile logistic operations and drayage, which involves transporting goods over short distances. In each of these cases, the routes are shorter, while usage schedules allow for scheduled off-time (usually overnight) charging. In addition, the weights of the loads are not as heavy, which makes these vehicles, according to one industry analyst, “the low-hanging fruit in terms of emission profiles.”34 Dedicated specialty service vehicles like sanitation and utility trucks have similar duty cycles, and so we are seeing more of these types of vehicles being introduced.

The case for EV adoption

With growing alignment in vehicle supply and an improving policy environment, the case for transitioning to electric vehicles grows even more compelling.

The primary external driver for doing so, of course, is to cut down on carbon emissions for the good of the planet. The faster and longer emissions rise, the greater the long-term increase in average global temperature. That, in turn, accelerates the frequency and severity of extreme weather, the rising sea-level and other costly, damaging impacts on the environment, wildlife, agriculture and human infrastructure.35

While this situation should concern everyone, it is the main driver for government action. As noted earlier, electrification of the transportation sector presents the potential for significant emissions reduction in support of Canada’s recently heightened international commitments under the Paris Agreement.36

There are other public policy benefits to electrification, too. In urban environments, for example, more EVs will lead to less noise and ground-level air pollution from trucks and cars.37 One recent study of the Greater Toronto Area and Hamilton region found that the air quality improvements achieved by significant transportation electrification could prevent hundreds of premature deaths annually and lead to billions of dollars in social benefits.38

Decision-makers who run companies involved in transportation and supply chain sectors value these external benefits, too. However, their rationale for investing in fleet electrification must be driven, first and foremost, by the business case. Fortunately, the two can go hand-in-hand. Many customers and investors now prefer to support companies with climate-friendly business practices.39 This means early adopters, which are converting fleets to electric today, may find It helpful to win contracts and attract new clientele tomorrow – even at a pricing premium. Also, as cities begin to impose emissions penalties on ICE-powered trucks or move to ban them entirely, an electric fleet becomes essential.40

However, the numbers must also add up. And increasingly, they do. At this stage, upfront expenses with electric trucks are still significantly higher than those of the conventional diesel and gasoline-powered vehicles. The upfront costs include both the vehicles themselves and the charging infrastructure. However, once the total cost of ownership over the vehicles’ lifespan is factored in, the balance increasingly tips in favour of EVs due to cost savings and lower maintenance expenses.41 Electricity is much cheaper than carbon fuel and electric vehicles have far fewer parts and require much less overall maintenance.

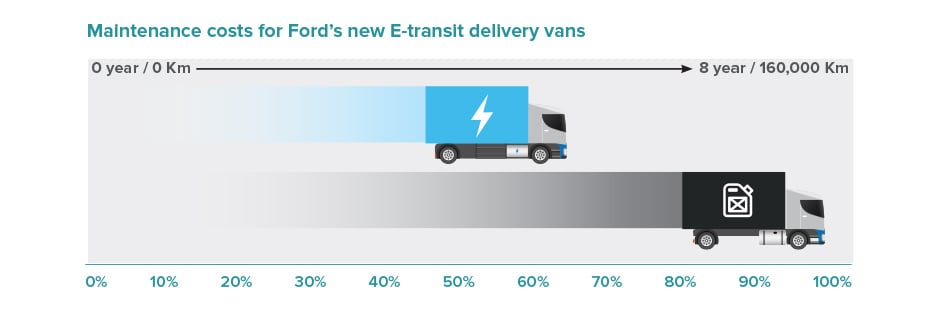

Maintenance costs for Ford’s new E-transit delivery vans

One example: Ford predicts that maintenance costs for its new E-transit delivery vans, available in North America as of late 2021, will be 40% less than the gas-powered equivalent over an eight-year/160,000-kilometre vehicle lifespan.42 The validity of that differential is also supported by large-scale, independent studies. In 2020, Geotab, an industry-leading fleet tracking and management service firm, assessed the EV suitability for 179,000 vehicles in use at 3,500 North American companies and concluded that more than 60% of fleet operators were losing money by not electrifying — even before any benefits from EV vehicle subsidies were included.43

It is also important to note that EV cost advantages will further strengthen as battery technology advances and prices continue to fall. Between 2010 and 2020, lithium-ion battery pack prices dropped by 89%, according to Bloomberg New Energy Finance (BNEF), with the average cost estimated at US$137/kWh.44 BNEF expects the average price to reach US$100/kWh in 2023 and to go as low as US$58/kWh by 2030.45 Vehicle manufacturing costs will be further dampened as production volumes increase. Vehicle buyers can also look forward to lower infrastructure prices and/or better services from utilities and other charging networks as their offerings mature.

While costs may come down, it is also important that companies become early adopters of EV technology rather than waiting until others have transitioned their fleets. It is the early adopters that will be the first ones to strike partnerships with businesses that recognize the benefits of going greener. The public is also keeping a close eye on which operations are taking climate change seriously and will reward those that are boldly moving in the right direction.

Depending on the business, early adopters will also get first access to subsidies, such as Canada’s iZEV program, which provides up to $5,000 in rebates to EV buyers. But these incentives will not last forever. Furthermore, few organizations can turn over their entire fleet all at once, which means companies should start making that transition to electrification now.

What is right for businesses?

Even as the macro business case increasingly favours electric trucks over gasoline and diesel, those in the for-hire transportation industry or companies that operate private fleets, must look carefully at their own fleet profiles, duty cycles and a host of other factors to determine their best EV strategy.

As noted, the current menu of EVs in the market favours certain classes and usage profiles, so, many companies will find it makes sense to start the transition with the parts of their fleet that can be most readily replaced.

A phased approach, perhaps starting with a modest pilot, also serves to develop first-hand understanding of how electric vehicles perform within business operations. Everyone in the organization, from drivers to maintenance workers to finance, will be on a learning curve and need time to grow comfortable with the new technology. Typically, familiarity brings satisfaction: once people are used to EVs most drivers report that they are more comfortable, cleaner and quieter to operate. A gradual transition also lessens the risk of unwelcome service disruptions for a company’s customers.

Another important consideration: while each business case will be unique, companies are not in this alone. Metro Supply Chain discovered this after talking to peers and seeking advice from industry experts. It was a relief to know that others were also thinking about their own transitions to EVs. It is beneficial to talk to others, both informally and through industry associations, and seek out user groups and consultancies that can help through the transition. Companies should ask questions: what kind of charging set-up works best? Is it most beneficial to lease or buy vehicles? This is also where it is important that governments at all levels, along with utilities, do their part to ensure supportive policies, end-user outreach, vehicle infrastructure and a robust electricity grid are in place.

While the climate crisis adds an urgency to this transition, transitioning to EVs is still a process. Metro Supply Chain’s purchasing decision tree followed the following line of thinking:

First and foremost, we wanted to determine if converting our fleet to electric vehicles was the right path. We looked at our customers: were they willing to pay a potential premium? Would they support us in this venture? Can we make a business case given the higher upfront costs? We were fortunate to have a customer willing to partner with us in the venture.

We determined how we were going to fund the project and presented our business case to the senior staff to gain support. Buy-in from the executive teams and the company as a whole is imperative to ensure the move toward electrification is embraced.

Once we were determined to go down the path of fleet electrification, we reviewed which trucks to purchase. When assessing costs, we looked at the entire lifecycle. Since Metro Supply Chain has a large geographical footprint, we ensured our vehicles were placed in a province that offered subsidies. We also reviewed the federal incentives, making sure to allocate enough time to the application process. We did not get it right the first time, but we stayed in touch with the approvers and incorporated their feedback when we resubmitted.

We analyzed our charging needs and the supporting infrastructure extensively. We ensured that the chargers would have the ability to charge the trucks in the time they were not in use and support the vehicles we purchased. We took into consideration the operational flexibility that would be required to ensure our business could operate with the new limitations that impacted route distances, hours of service, load weights and dimensions, tailgate usage, outside temperatures, and cab temperature control.

Not only did we need to ensure that the chargers would support the vehicles we purchased and be able to charge the trucks in the time they were not in use, we also needed to ensure they would support the technology advancements of trucks we might purchase in the future as we continue to expand our fleet.

As we progressed in establishing our infrastructure, we found ourselves in a dilemma — we were in the midst of moving warehouse locations, so installing the chargers in one location only to be taken down and reinstalled in another would be costly. Working with our advisors, we developed a custom mobile charging station that can easily be moved and supports our changing business needs.

The solution itself included a retrofitted container with the chargers affixed to the outside for ease of truck access. Furthermore, due to the evolving electrification environment and the necessity to be flexible to meet our clients’ needs, mobile charging stations are becoming a more viable option for Metro Supply Chain’s infrastructure.

We did not overlook the importance of driver and operations training. Though EVs fundamentally drive like their ICE counterparts, there are key differentiators that require further training in order to ensure optimal vehicle performance, longevity and to minimize the risk of damage. For example, learning how to correctly use the acceleration and brake peddles can increase vehicle range.

Conclusion

In the long term, the move to EVs is inevitable, which is why companies across the supply chain need to start transitioning their fleets. Shifting to an all-EV operation takes time and resources, but businesses that commit to the journey sooner will be rewarded. Metro Supply Chain took this approach. While we are in the early stages of our journey, we are already supporting a global retailer that provides significant last-mile delivery, making our collective impact that much greater with more partnerships to come.

We are also taking advantage of the available government incentives, which is making our transition more affordable. By learning from our achievements and missteps now, we are in a much better position for long-term success. If this white paper helps others learn from our efforts and more easily launch their transitions, then we, as a human race, will be one step closer to meeting the world’s climate goals.

10 ways to strengthen Canada’s zero-emission vehicle (ZEV) freight sector

1. UNIFY ZEV STRATEGIES

Co-ordinated ZEV strategies for commercial vehicles among companies and countries, along with associated long-term investment plans, will promote uptake within fleets. Sales mandates for medium- and heavy-duty vehicles are effective tools in speeding up the transition to clean freight delivery.

2. SHARE COSTS ACROSS INDUSTRIES

If Canada is going to meet a target of 25,000 new zero-emission medium- and heavy-duty vehicles by 2025, it will need to invest billions of dollars, including $5 billion for vehicle procurement alone. This becomes more affordable if costs are shared across all sectors.

3. GET MORE INSIGHT INTO GOVERNMENT PLANS

The industry must have more transparency and certainty into the long-term renewal of government financial incentives. If companies know that incentives are continuing, then they’ll be better able to plan their transition to ZEV over time.

4. OFFER PREFERENTIAL TREATMENT TO ZEV

Governments should consider expanding non-financial mechanisms, such as green licence plate programs that give preferential treatment to commercial zero-emission vehicles. That would further encourage the transition to low-emission fleets.

5. RESTRICT TRAVEL OF HIGHER POLLUTING VEHICLES

Commercial fleet operators would be more likely to move to ZEV fleets if municipalities restricted the travel of high-polluting vehicles (at least over time) and set emission reduction targets that align with Canada’s decarbonization goals.

6. IMPLEMENT CURBSIDE MANAGEMENT TACTICS

Municipalities should also consider implementing curbside management tactics, such as allowing for deliveries during off-peak hours and regulating what types of vehicles can stop at loading zones.

7. INVEST IN INFRASTRUCTURE

Much of the EV discussion has been around emission targets and getting more vehicles on the road.

The government must expand on its investment in infrastructure. If 25,000 new zero-emission medium- and heavy-duty vehicles are in use by 2025, a $350-million investment in charging infrastructure will be required.

8. CREATE MORE TARGETED INCENTIVE PROGRAMS

Provincially created charging infrastructure incentive programs would be more useful if they were expanded to directly target freight vehicles, with flexibility for private, single-use access, and to ensure coverage of higher-powered stations.

9. CO-ORDINATE ON INFRASTRUCTURE BUILDOUTS

Developing publicly accessible charging stations along national highways or provincial and municipal roads could be done in co-ordination with a variety of stakeholders in the goods-movement sector, so that everyone’s charging needs are kept in mind. Also, encourage early adopters in the transport sector to work together to share charging infrastructure. The greater the collaboration, the more the needle can move.

10. SUPPORT JOBS

For EV adoption to happen in earnest, investments into transportation-related labour market programs must be made. The industry needs to support good paying jobs if it is going to deploy and maintain ZEV fleets, especially as the sector moves to scale up to mass adoption.

Glossary

TRUCK CLASS DUTY CLASSIFICATION WEIGHT LIMIT

Class 1 Light duty 0–6,000 pounds (0–2,722 kg)

Class 2a Light duty 6,001–8,500 pounds (2,722–3,856 kg)

Class 2b Light duty 8,501–10,000 pounds (3,856–4,536 kg)

Class 3 Light duty 10,001–14,000 pounds (4,536–6,350 kg)

Class 4 Medium duty 14,001–16,000 pounds (6,351–7,257 kg)

Class 5 Medium duty 16,001–19,500 pounds (7,258–8,845 kg)

Class 6 Medium duty 19,501–26,000 pounds (8,846–11,793 kg)

Class 7 Heavy duty 26,001–33,000 pounds (11,794–14,969 kg)

Class 8 Heavy duty 33,001 pounds (14,969 kg) and above

Endnotes

1. https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_SPM.pdf

4. https://www.blackrock.com/corporate/investor-relations/larry-fink-ceo-letter

5. https://www.wemeanbusinesscoalition.org/ambitious-u-s-2030-ndc/

https://www.theglobeandmail.com/business/article-net-zero-emissions-pledges-by-canadian-companies/

8. https://www.pembina.org/pub/building-zero-emission-goods-movement-system

11. https://theicct.org/publications/second-ghg-standards-hdv-Canada

12. https://globaldrivetozero.org/2019/05/28/vancouver-announcement/

15. https://www.pembina.org/pub/building-zero-emission-goods-movement-system

17. https://cleanbc.gov.bc.ca/

18. https://www.transportdive.com/news/electric-class-8-trucks-battery-hydrogen/593512/

19. https://www.driveelectricvt.com/blog/winter

20. https://electricautonomy.ca/2021/09/22/election-2021-climate-crisis-denial/

22. https://liberal.ca/our-platform/zero-emissions-vehicles/

23. https://www.nescaum.org/topics/zero-emission-vehicles

24. https://calstart.org/zet-statement-of-principles-6-17-20/

26. https://www.greenbiz.com/article/2021-year-electric-trucks

28. https://electricautonomy.ca/2021/09/21/kruger-energy-peterbilt-electric-truck/

29. https://electricautonomy.ca/2021/09/11/kenworth-electric-truck-camionnage-canada/

30. https://www.transport-magazine.com/groupe-morneau-lacquisition-de-premier-camion-electrique/

32. https://www.yahoo.com/now/electric-trucks-market-estimated-69-075400935.html

33. https://runonless.com/wp-content/uploads/RoL-E-Infographic-HZ.pdf

34. https://electricautonomy.ca/2020/10/30/zev-commercial-vehicle-supply/

35. https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_Headline_Statements.pdf

36. https://pm.gc.ca/en/news/news-releases/2021/04/22/prime-minister-trudeau-announces-increased-climate-ambition

37. https://www.mdpi.com/2071-1050/12/3/1052/pdf

39. https://news.cornell.edu/stories/2020/03/execs-consumers-pushing-companies-toward-sustainability

40. https://electricautonomy.ca/2021/06/24/7-generation-capital-fleet-evs/

41. https://blog.fleetcomplete.com/how-will-electric-vehicles-impact-the-trucking-industry

42. https://www.fleetequipmentmag.com/electric-vans-last-mile-delivery/

43. https://www.geotab.com/blog/ev-suitability/

44. https://about.newenergyfinance.com/electric-vehicle-outlook/